In the realm of real estate, it is important to take into account the significance of closing costs when purchasing a property in any place.

Closing costs are something every buyer and seller should be aware of, especially if you plan on buying or selling a house in a thriving city like Sunnyvale, CA. Whether you’re a buyer or seller, knowing what to expect in terms of closing fees will give you peace of mind and help you make smart choices throughout the transaction.

In this article, we will discuss the various components that comprise the Sunnyvale, CA, closing costs of all parties involved in a real estate deal.

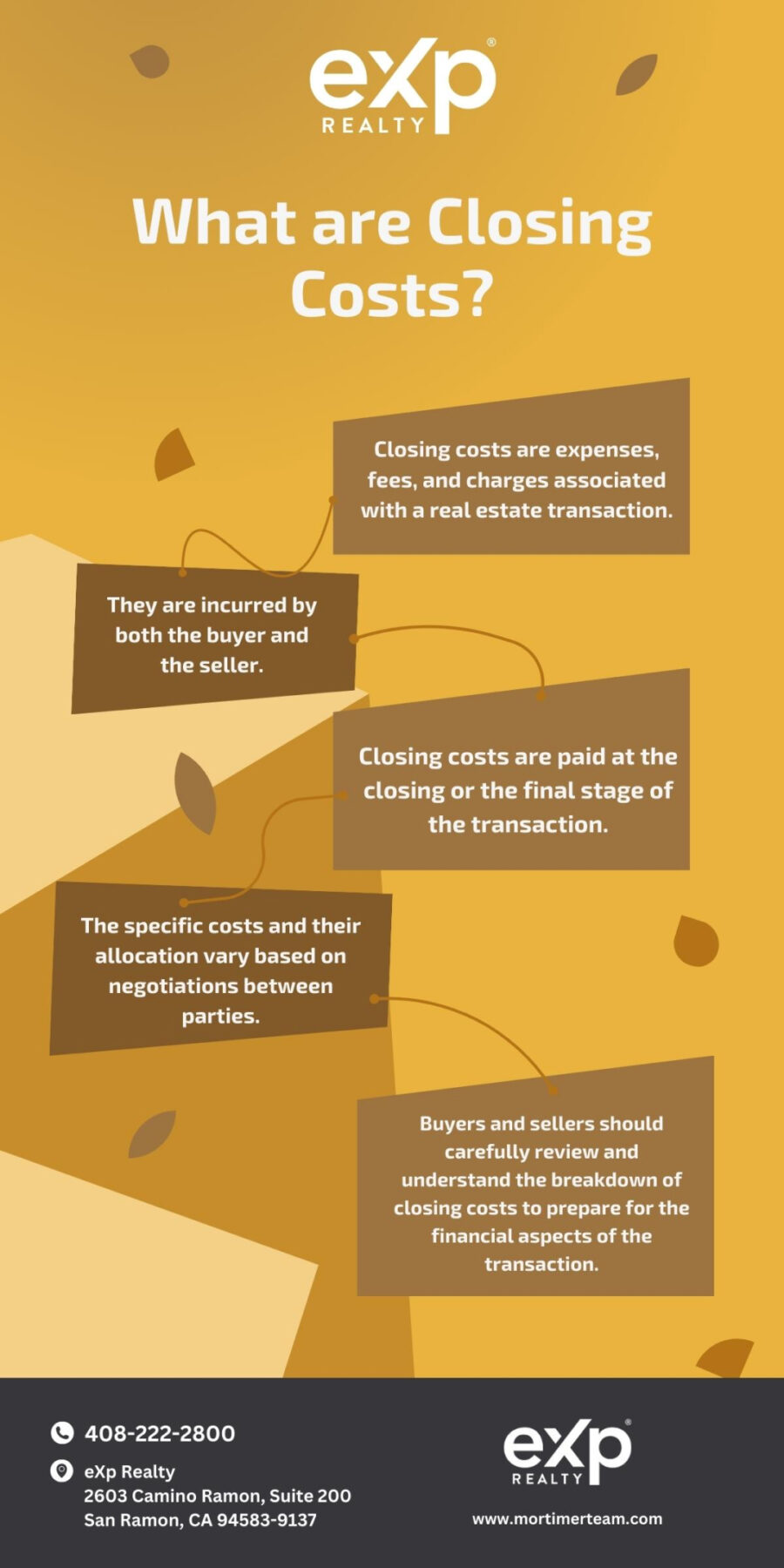

Closing costs encompass fees and expenses associated with the transfer of home ownership during the final stages of a real estate transaction. These are customary expenses shared by the buyer and seller and vary between every deal, often based on factors such as the property’s location, type, and transactional terms.

The real estate market of Sunnyvale, CA, is currently experiencing a high level of competition. Because of this, closing costs in the city are also high compared to other areas in the state.

According to recent statistics, the median sale price of a home in Sunnyvale experienced a 0.5% increase compared to the previous year, reaching approximately $1,900,000. For properties falling within that price range, the estimated Sunnyvale, CA closing costs would most likely range from $19,000 to $57,000, representing at least 1% to 3% of the total sales price.

Under California law, a personal appearance by the buyer and seller at the closing table is optional.

It is mainly because real estate agents and brokers are commonly relied upon as intermediaries between buyers and sellers. They will be the ones to ask inquiries and negotiate terms on each party’s behalf.

In California, unlike most other jurisdictions, a real estate agent can represent both parties.

This arrangement, known as dual agency, allows a single agent or brokerage to work with both parties involved in the sale. Both the buyer and the seller must give their written approval for the transaction to go through. The brokers and agents engaged in the real estate transaction will be listed on the Disclosure Regarding Real Estate Agency Relationships form you will fill out.

Property taxes in California have been limited to 1% of the purchase price since 1978 in accordance with Proposition 13.

How Much Are Closing Costs for Buyers in California?

Closing costs are divided between buyers and sellers, but the amount they pay differs.

We have prepared a list of some of the typical closing costs shouldered by the buyer in a real estate transaction in California to help you prepare financially through your home-buying journey:

Closing Cost

Description

Amount / Range

Application Fee

The application fee is intended to pay the costs of processing the borrower's application. It may include things like reference checking.

Note: Application fees vary widely from lender to lender. This cost is also normally non-refundable even if your loan application is declined or you decide not to proceed

Varies

Appraisal Fee

An appraisal is performed to determine the current fair market value of a property.

Mortgage lenders require home appraisals to ensure the property's value aligns with the loan amount.

The appraisal fee pays for the services of a certified appraiser to conduct an objective analysis of the property and determine its fair market value.

$300 to $600

Credit Fees

These fees are associated with checking and evaluating the borrower's credit history and creditworthiness.

It covers the cost incurred by the lender for obtaining the borrower's credit report from one or more credit bureaus.

Varies

Home Inspection Fee

A trained expert will evaluate the property's overall condition during a house inspection.

It includes assessing the foundation, wiring, plumbing, air conditioning, heating, ventilation, roof, and general security.

The inspector will provide you with a full report of his findings, including notes on any problems and recommended fixes.

Note: Although not required by law, having a home inspected is a smart idea before making a significant purchase.

$335 to $500. However, the cost may be higher for larger or more intricate properties.

Origination Fee

Lenders often charge an origination fee to set up your loan.

This fee typically covers underwriting, document preparation, and other origination-related administrative procedures.

Note: Make sure to compare this cost among different mortgage lenders in your area since it can vary significantly.

Varies but usually costs around 0.5% to 1% of the total loan amount.

Mortgage Points

Borrowers pay mortgage points to their lender in exchange for a reduced interest rate and a lower total interest paid over the life of the loan.

Buying points often results in a 0.25% reduction in your loan's interest rate.

Here's How It Works: For example, you need to borrow $300,000, and your prospective lender proposes a 4% interest rate with no discount points. You may be able to get your interest rate reduced from 4% to 3.75% if you pay one mortgage point up front, which is equal to 1% of the loan amount, or $3,000 in this case. Throughout the loan, this could mean cheaper monthly mortgage payments.

1% of the loan amount

Property Taxes

Buyers may need to prepay property taxes during the home purchase.

The prepaid amount can vary from six months to a year, depending on the specific circumstances.

Note: While some closing costs may be negotiable, note that taxes are not. So, it would be best if you will also consider property and transfer taxes, especially in California, where both are applicable.

Varies

Title Fees

Title fees safeguard the buyer and lender against any claims against the property's title through a title search and title insurance.

It typically includes the title search fee, title examination fee, closing or settlement fee, and the cost of the title insurance policy.

Search: $75 to $200

Insurance: 0.5% to 1.0% of the sale price

How Much Are Closing Costs for Sellers in California?

Seller closing expenses in California might differ depending on several factors, such as the transaction’s specifics and the terms the buyer and seller agreed upon.

Some of the typical seller closing charges in California are as follows:

Closing Cost

Description

Amount / Range

Document Preparation and Recording Fees

Sellers are responsible for fees associated with preparing and recording the necessary documents to finalize the sale.

These fees can vary but are generally in the range of a few hundred dollars.

Escrow and Title Fees

Sellers often share specific escrow and title fees with the buyer.

These fees include the cost of opening an escrow account, conducting a title search, issuing a title insurance policy, and facilitating the transfer of ownership.

Flat rate of $350 plus $1.75 for every $1,000 of the home's purchase price.

Prorated Property Taxes and HOA Dues

Sellers may need to reimburse the buyer for a portion of the property taxes and homeowners association (HOA) dues that have been prepaid beyond the closing date.

Varies depending on the closing date and the payment schedule of the taxes and HOA dues.

Real Estate Commission

The most significant portion of closing costs for sellers is usually the real estate commission.

The commission is divided between the listing agent and the buyer's agent.

Varies, but usually costs around 5% to 6% of the sale price.

Transfer Taxes

Sellers in California are responsible for paying transfer taxes, which are calculated based on the sales price or assessed value of the property being transferred.

Varies

Note that these are just some of the typical closing costs for sellers in California. Other potential costs may include home warranty premiums, repair credits, and any outstanding liens against the property.

Note: This image may include elements generated by artificial intelligence (AI).

Conclusion

Sunnyvale, CA, closing costs are an essential part of the home-buying process in the city. Because of this, it is important to be aware of them and plan your finances accordingly.

Although these costs are inevitable, there are ways to minimize closing costs. However, keep in mind that negotiating closing costs is a matter of agreement between the parties involved and depends on market conditions and individual circumstances.

Sunnyvale, CA, may have specific requirements or customary practices that differ from other areas. It is advisable to work with local real estate professionals that are familiar with the local market to understand and give you more accurate estimates of closing costs for buyers and sellers in California.

We hope this article gives you a clearer idea of what closing costs in Sunnyvale, CA are and helps you to lay out your financial plan accordingly. If you are interested to learn more about the lovely residential communities in Sunnyvale, CA, please feel free to contact one of our market specialists to get started.

You may also join our online community to know the latest trends and updates about Sunnyvale, CA, and connect with other members who share similar interests!

Closing costs in California usually cover expenses related to inspection, appraisal, and origination, in addition to title insurance, courier fees, and taxes.

Additional expenses such as mortgage insurance, flood certification, and HOA or condo fees may also be required.

Closing costs are divided between the buyer and the seller. However, the specific allocation of total costs may vary depending on the terms agreed upon in the real estate contract.

Closing costs for a seller in California can be challenging to estimate without knowing specifics about the buyer’s financing, the seller’s financial situation, and other variables.

The terms agreed upon by the parties involved also affect the total closing costs. A more precise estimate of your closing costs can be obtained by consulting a real estate agent or attorney versed in California real estate transactions.

Post author:

Charles Mortimer

Post author:

Charles Mortimer